Portfolio Strategy: February 23, 2026

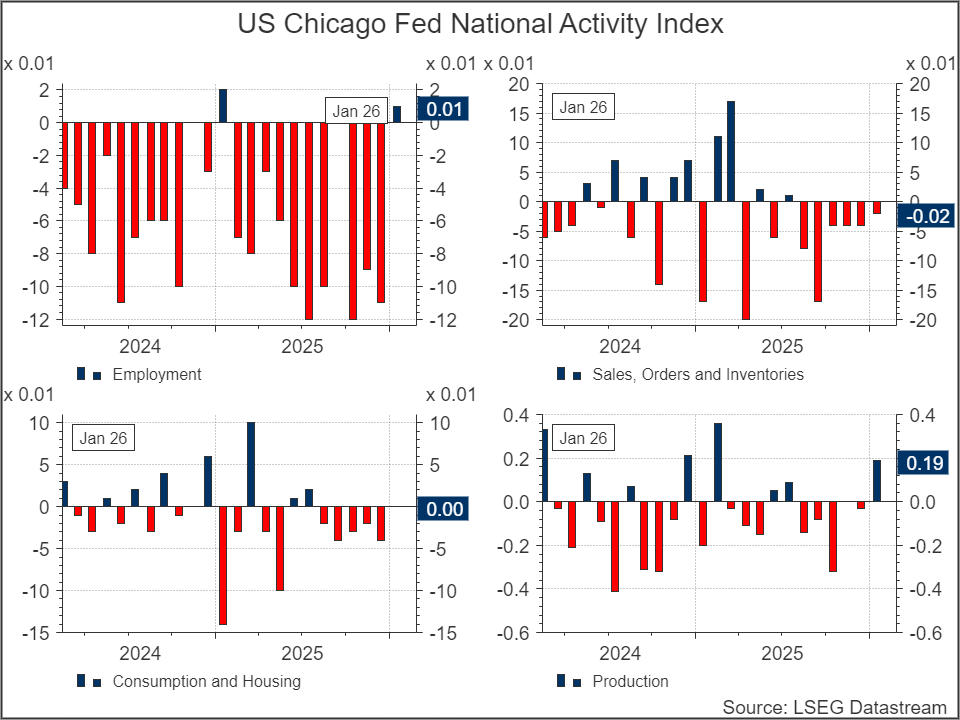

Chicago Fed Activity Index Turns Positive in January

The Chicago Fed National Activity Index rose to +0.18 in January 2026 from -0.21 in December, marking its highest level since February 2025 and signaling a pickup in US economic activity at the start of the year.

Production-related indicators drove the improvement, contributing +0.19 compared with -0.03 previously, while employment indicators edged up to +0.01 from -0.11. The sales, orders, and inventories category remained slightly negative at -0.02, though improved from -0.04, and personal consumption and housing made a neutral contribution after subtracting -0.04 in December.

Source: Trading Economics.

Take Five: Nvidia earnings head for centre stage

Feb 20 (Reuters) - Nvidia's earnings report is this week's centrepiece for markets, flanked by important data and politics in Europe, where both politicians and central bankers are jostling for top jobs.

A U.S. Supreme Court ruling from late Friday striking down key parts of President Donald Trump's tariff plans will also add a dose of volatility to markets as investors and companies try to get a handle on what goods will be taxed, at which rates, and from which exporting countries.

Here's all you need to know about the week ahead in financial markets from Lewis Krauskopf in New York, Rae Wee in Singapore, and Marc Jones, Harry Robertson and Dhara Ranasinghe in London.

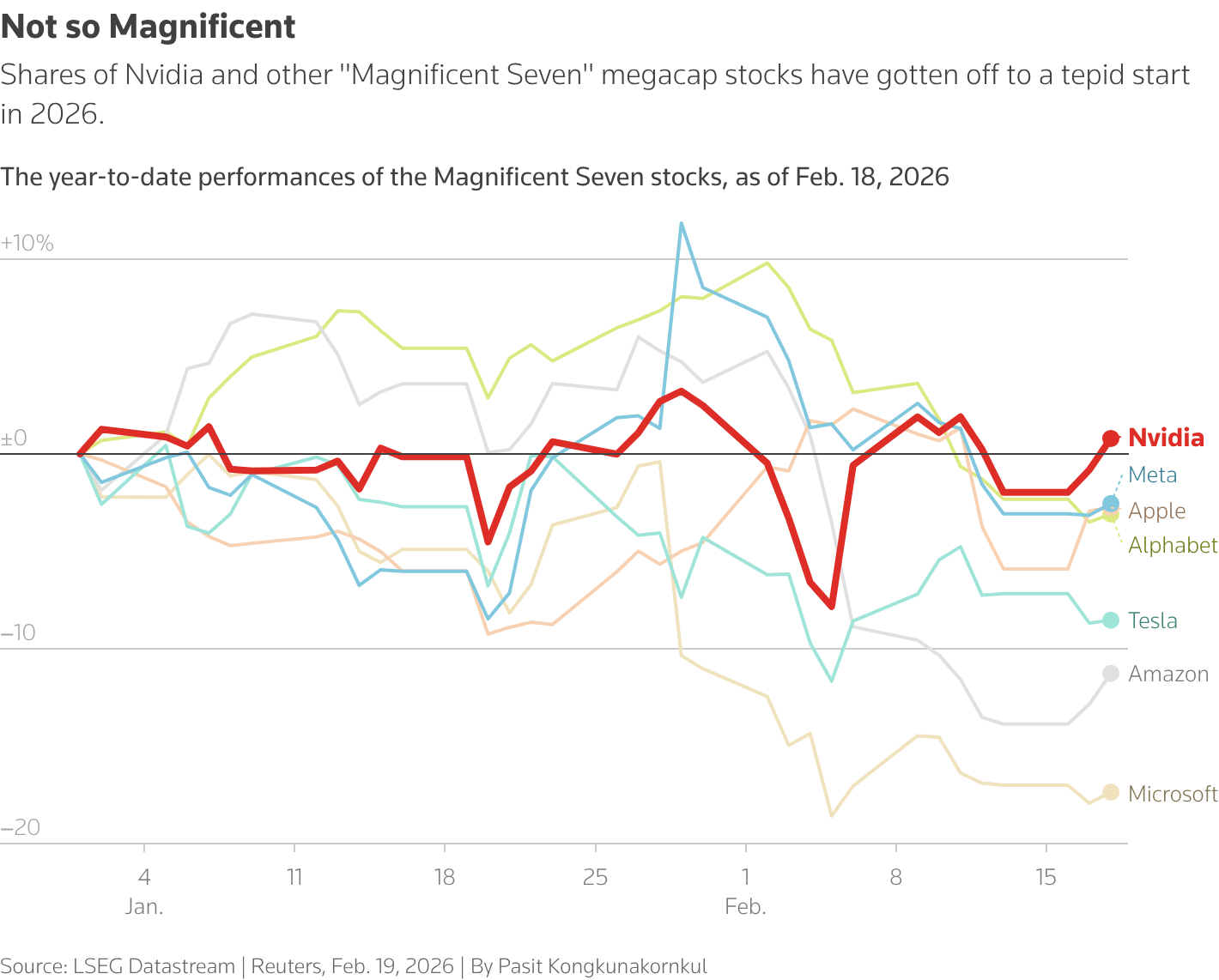

1/ NVIDIA'S MOMENT

Artificial intelligence bellwether Nvidia NVDA.O is set to post quarterly results as investors worry about returns on AI spending and industry disruptions caused by the emerging technology.

Wednesday's report from the semiconductor giant, the world's largest company by market capitalization, will be a major event for stock markets. Nvidia shares have soared following the launch of ChatGPT in late 2022. Still, shares of the company and other "Magnificent Seven" megacap stocks have stalled so far in 2026.

Investors will also focus in the coming week on earnings reports from software companies including Salesforce

CRM.N and Intuit INTU.O. Software stocks have been hammered this year over concerns AI will lead to upheaval for the industry's business models.

2/ ANNIVERSARY ANGST

Tuesday marks the fourth anniversary of Russia's full-scale invasion of Ukraine, and though U.S. President Donald Trump's push for a ceasefire continues, getting one over the line remains devilishly difficult on all sorts of fronts.

Ukraine has faced sustained pressure to agree to a deal that could mean painful concessions, as Russian forces pound its power grid and slowly advance on the battlefield.

At the same time, the International Monetary Fund looks set to rubber-stamp extended support, meaning Kyiv's bonds are flying high.

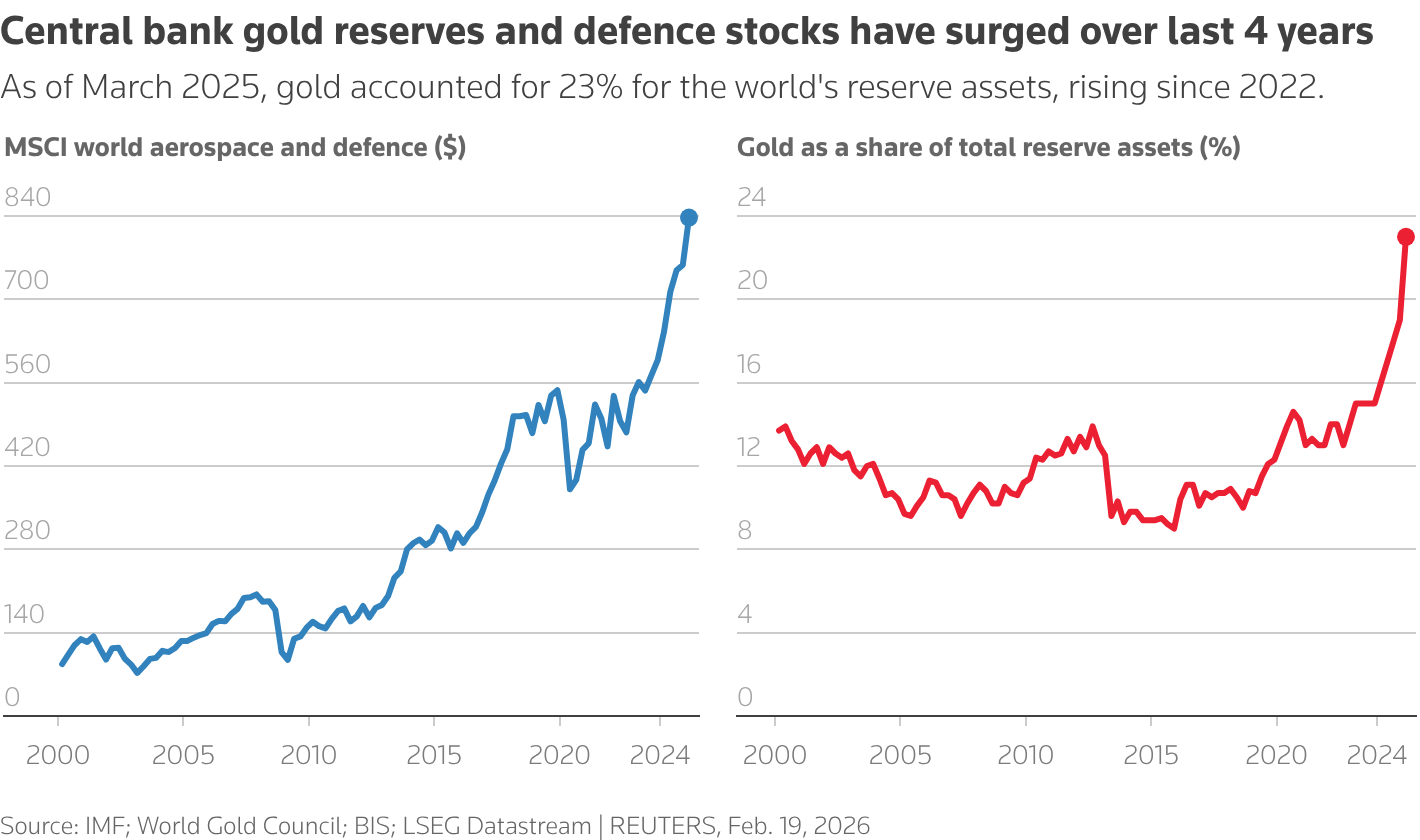

As volatile oil prices show, markets are also grappling with the potential of U.S. military action against Iran amid the long-running dispute over Tehran's nuclear abilities. Defence stocks and gold have also been beneficiaries.

Add in this year's Greenland and Venezuela flashpoints and the tinderbox situations in Gaza, Africa and Taiwan, and analysts warn of an everything, everywhere, all at once era of geopolitical turmoil where one crisis rolls into the next..

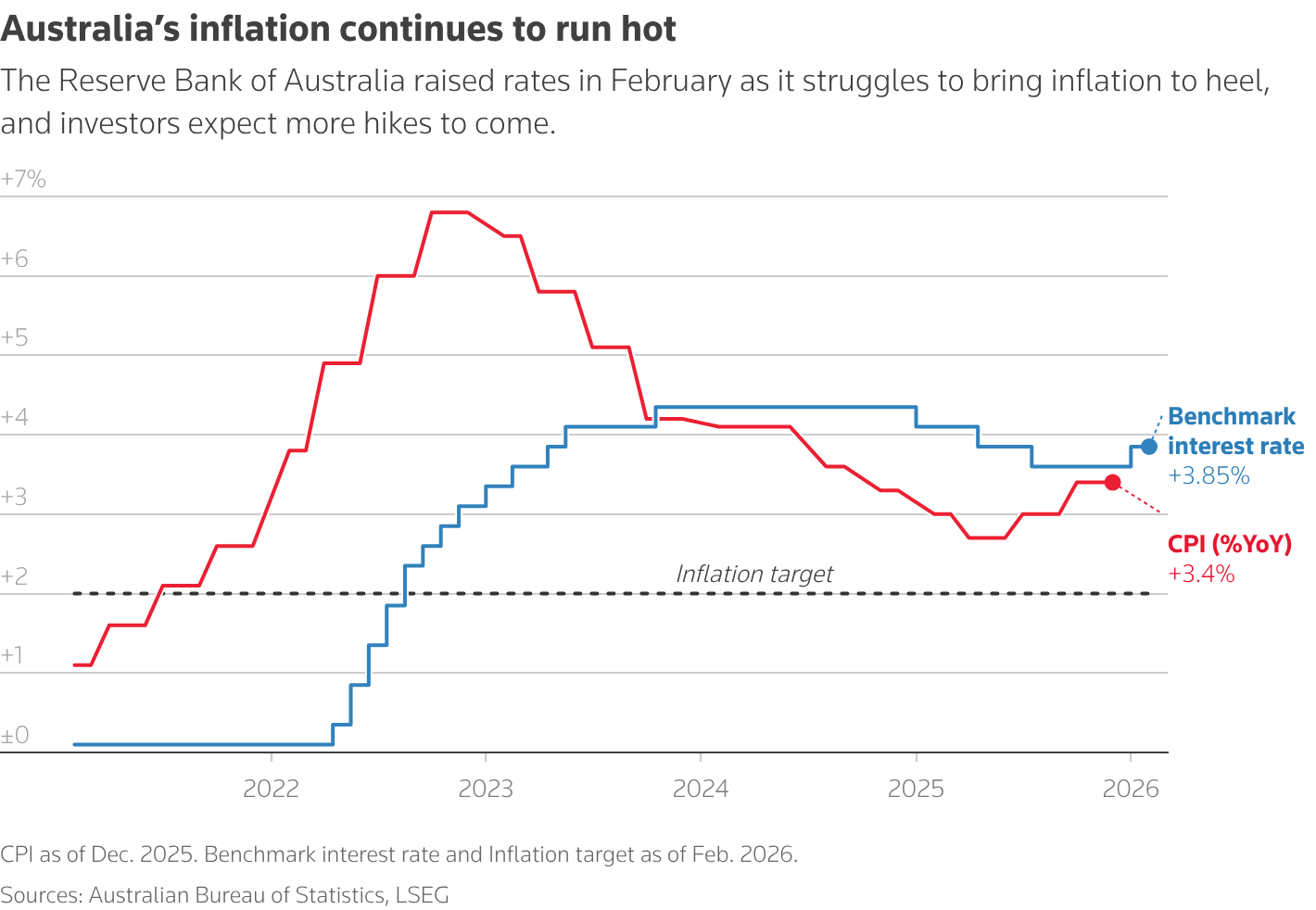

3/ STILL RUNNING HOT

Australia's consumer price reading due on Wednesday will be closely watched by investors, who are betting the central bank will hike rates at least once more this year as the economy remains in rude health and inflation proves sticky.

The Reserve Bank of Australia earlier this month became the only G10 central bank outside Japan to tighten policy, as it struggles to bring inflation under control in a supply-constrained economy.

Any upside surprise in Wednesday's figures would further cement bets that policymakers could deliver another 25 basis-point hike in May 0#AUDIRPR, bringing the cash rate to 4.10%.

Elsewhere in Asia, Tokyo's inflation data is due on Friday, though it's unlikely to materially alter the Bank of Japan outlook.

Analysts say Japanese Prime Minister Sanae Takaichi's historic election win clears the path for further BOJ tightening, leaving markets pricing in two rate hikes by December. 0#JPYIRPR.

4/ KEIR PRESSURE?

British Prime Minister Keir Starmer faces a reckoning on Thursday, when a Manchester one-off by-election could deliver a fatal blow to his faltering leadership.

Investors will be watching closely. Some fear a more left-wing successor to Starmer could ramp up spending and borrowing, adding to the flood of government bonds hitting markets.

British gilts and the pound wobbled earlier this month as a crisis engulfed Starmer over what he knew of Peter Mandelson's links to paedophile Jeffrey Epstein when he appointed the former as U.S. ambassador.

Markets calmed when Starmer's cabinet backed him, and recent UK bond sales have seen record demand as investors have snaffled up the sky-high yields on offer.

Should Labour get walloped by Nigel Farage's Reform or the Greens in the seat of Gorton and Denton, Friday could be another volatile day for British markets and Westminster.

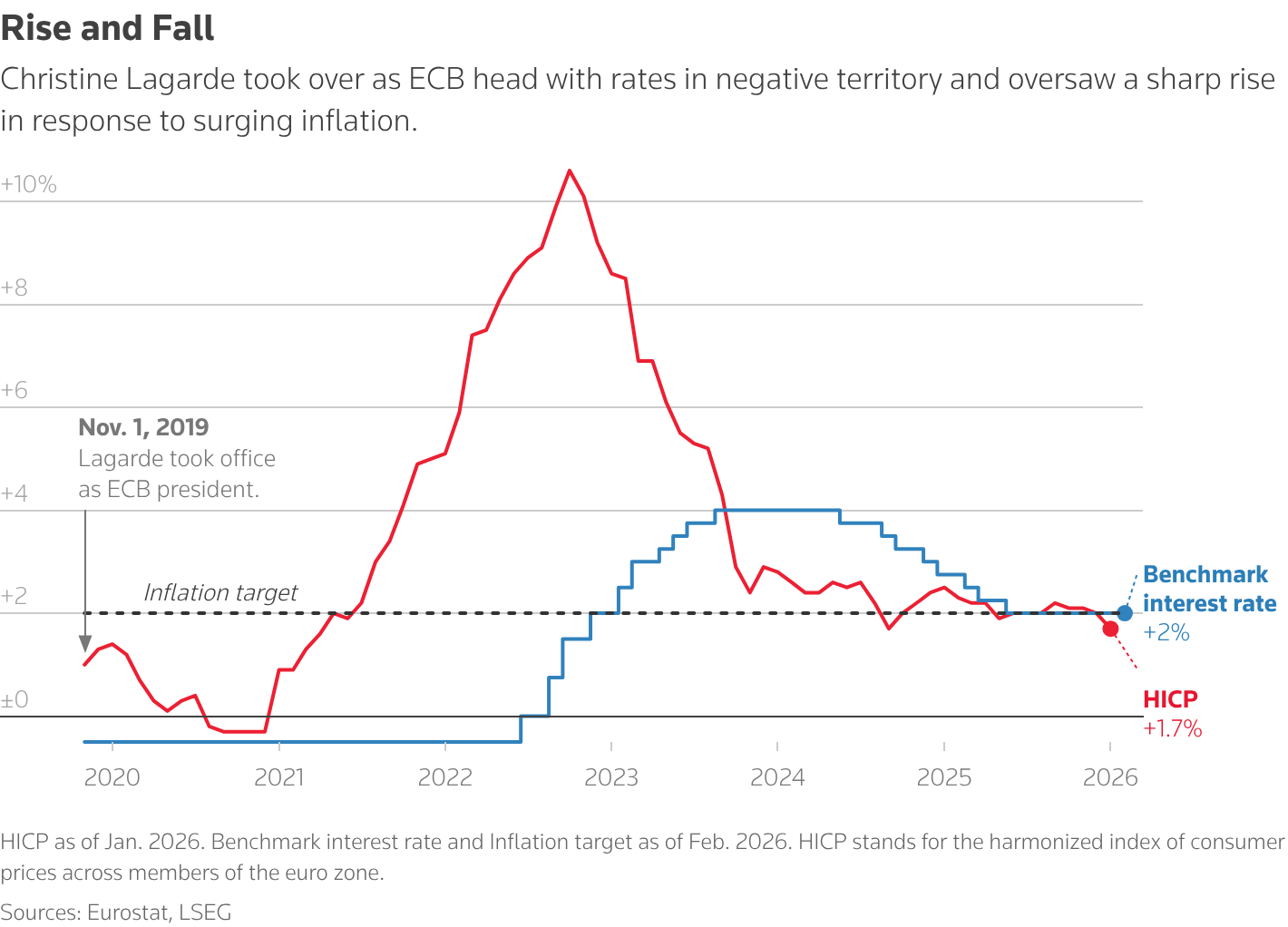

5/ MUCH ADO ABOUT NOTHING

An otherwise dull ECB outlook just got a bit of a spark following a Financial Times report that Christine Lagarde plans to leave her post as president early.

Lagarde told the Wall Street Journal she expects completing her mission as president of the ECB will take until the end of her term.

This all has traders focusing on succession at one of the world's most important central banks, at the same time as bracing for change at the Fed.

Lagarde leaving early, the FT says, is to give outgoing French leader Emmanuel Macron a say in picking her successor.

It's early days, and Friday's preliminary February German, French and Spanish inflation data will likely confirmsteady rates for the rest of 2026.

Still, a guessing game of who next leads the ECB is underway. And consider this: has central bank independence been compromised by politicians tempted to bend the rules to guarantee their pick of ECB chief?

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies.

Ventum Financial Corp. www.ventumfinancial.com

Vancouver Office

2500 - 733 Seymour Street

Vancouver, BC V6B 0S6

Ph: 604-664-2900 | Fax: 604-664-2666

For a complete list of branch offices and contact information, please visit our website.

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre - Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited.

For further disclosure information, reader is referred to the disclosure section of our website.